Entrepreneurs are not always aware of the different financing tools available to them when raising funding and which are the implications of the different forms of funding for their company. In this article, I will outline some of the different funding options available to startups and discuss their pros and cons.

Forms of funding available to startups

In a typical startup, the founders start by committing their own funds to kick-start the company at the time of incorporation. With these funds, the idea is further developed into a mock-up product and an elevator pitch with which to approach investors. It is not uncommon that friends and family jump in during this very first stage when the company is still working on its minimal viable product. With the first product in hand, the entrepreneur can go to business angels who typically invest larger amounts of about 50-100k per investor.

It is rare that the startup is able to generate high cash flow early on, and so the first business angels are often asked to reinvest several times more before the company gets its first solid revenues and is able to grasp the attention from a Venture Capital firm or even reach break even.

Fig. 1) Typical funding stages of a startup company

Raising funding through straight equity

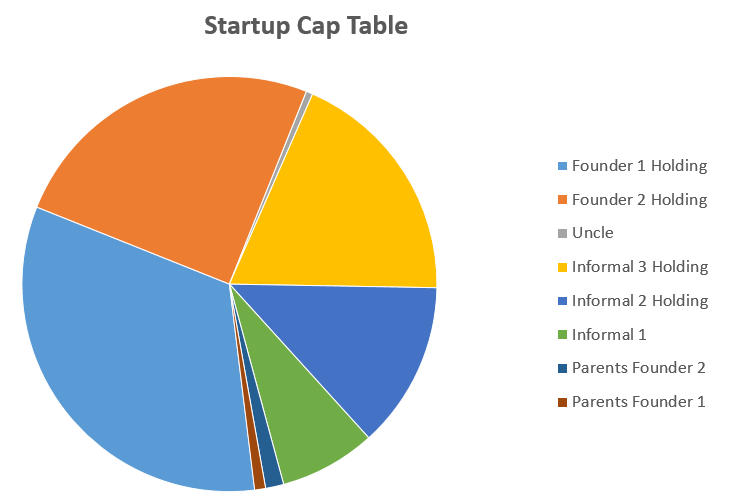

The most well-known form of raising funding is by means of straight equity. In a straight equity investment, the investors receive shares in the company for an agreed price. An additional shareholders’ agreement may outline additional rights which the shareholders receive. The initial termsheet will outline the deal terms, including valuation, and any special rights such as anti-dilution, liquidation preference, and certain blocking rights. However, early-stage investors will often have relatively few demands when it comes to these preferential rights. When a company issues shares directly for each investment, both friends, family and business angels will all have a place in the capitalisation (cap) table and thus also in the shareholders meeting.

Fig. 2) A cap table of an early-stage company containing both friends, family and business angels.

3 Considerations when raising funding through straight equity

There are three considerations when using straight equity. For one, it is costly to issue shares for each investment because of the notary and lawyers that are necessarily involved. Especially if the investment is small, transaction costs are a significant barrier. Costs of drafting a term sheet with an experienced lawyer may start at €1,000, a shareholder agreement can be as much as €3,000, and the share issuance by the notary can easily cost €1,000. In practice, these costs will be higher if there are unexpected developments or if the deal is more complex.

However, the main concern is that the accurate valuation of companies in a pre-revenue phase is close to impossible. The use of common metrics such as multiples and future cash flow projections will give highly uncertain results. The wrong valuation can create potential problems with future investors. For example, if the first valuation was set too high, and the new investors negotiate a lower valuation, the earlier investors will be upset. New investors often do not wish to risk a conflict with earlier investors, and will rather pass on the opportunity.

Finally, by issuing equity to each investor, the shareholders meeting will become over-crowded. Many corporate actions require a signature from each shareholder. The more investors you have holding straight equity the more complicated decision-making will become. Future investors may well see a crowded cap table as a red flag, and some future investors such as VCs, may decide not to invest.

To avoid using straight equity startup even sometimes use a loan agreement over equity for early-stage investment. Loan agreements keep the cap table clean, but they have the obvious downside that it creates a so-called ‘debt overhang’. That is, the loan will have to be repaid by the startup often before it makes a profit. This money will then have to come from future investors, who wish to invest in the development of the product rather than in the repayment of a loan.

Raising funding with convertible notes

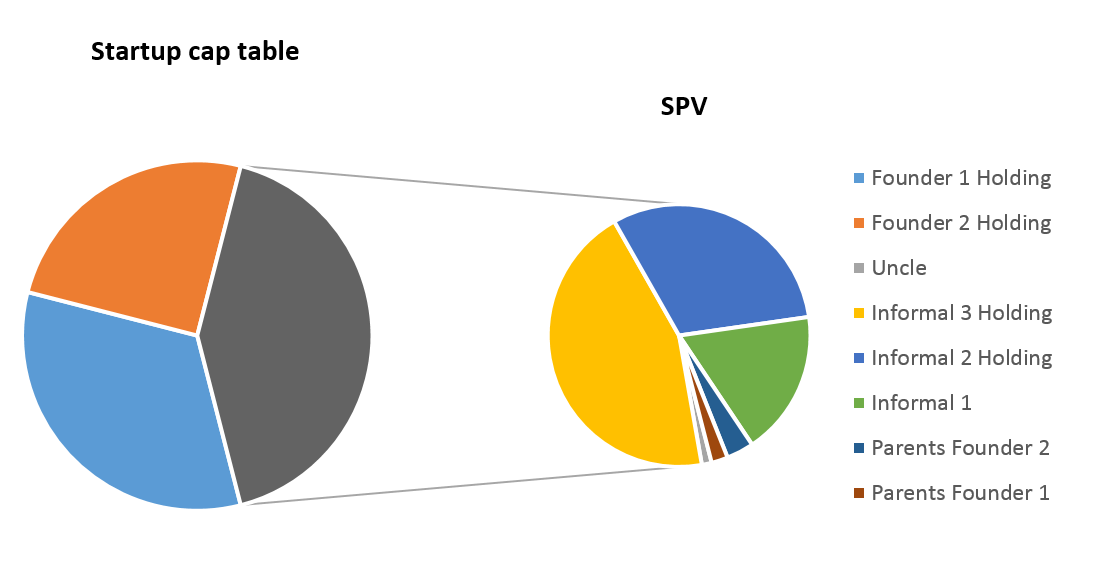

Because of the challenges with early-stage investing in shares the convertible note was invented. Convertible notes are debt instruments with an interest rate, but with an up-front agreement that the outstanding loan will convert into equity at a given time. If you have multiple investors, the startup and investors can agree to convert the into depositary receipts in a special purpose vehicle (‘SPV’). The benefit of this is to pool the investors into 1 entity, which keeps the cap table clean. The investor pool can be formed as a special purpose vehicle: in the Netherlands traditionally the ‘Stichting Administratiekantoor’ (‘StAK’) is used for this purpose, while in Germany and elsewhere it is common to use a limited liability partnership structure such as a K.G. The structure represents all the investors but has only one representative in the shareholders meeting.

Fig. 3) A cap table of a company where the convertible notes have been converted into depository receipts in an SPV.

The convertible note usually has a final conversion date or converts when a Series A investment occurs. In this case, the share price used for conversion is the share price paid during the Series A investment. In order to reward the convertible note investors for investing early, they will receive a discount to this share price. This way the valuation is aligned with the new investor and upside is provided for investing early.

Convertible debt has become a very popular and common tool for investing and startups in the US. According to Paul Graham from Ycombinator, every investment made during his latest batch has been made using convertible notes.

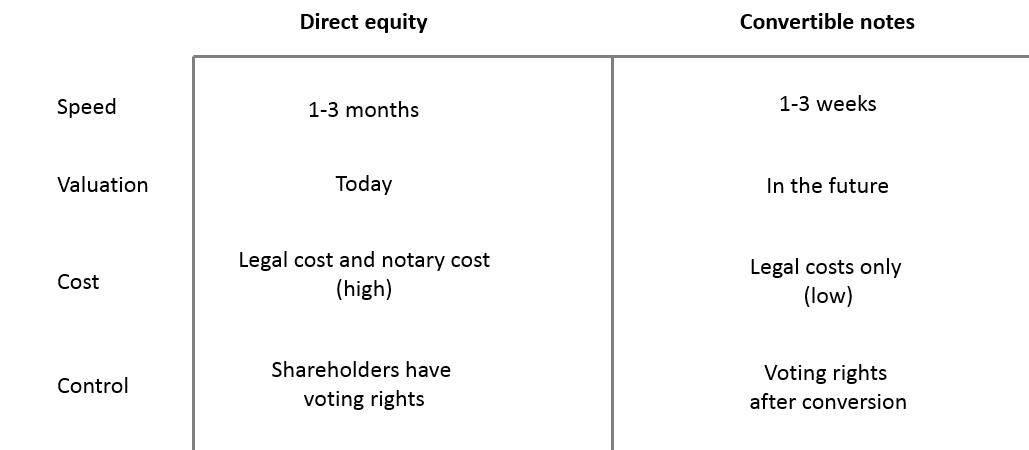

The following table shows a comparison of some important features of funding with straight equity vs. convertible notes.

Fig. 4) Comparing straight equity vs. convertible notes

Log in with Linkedin

Log in with Linkedin